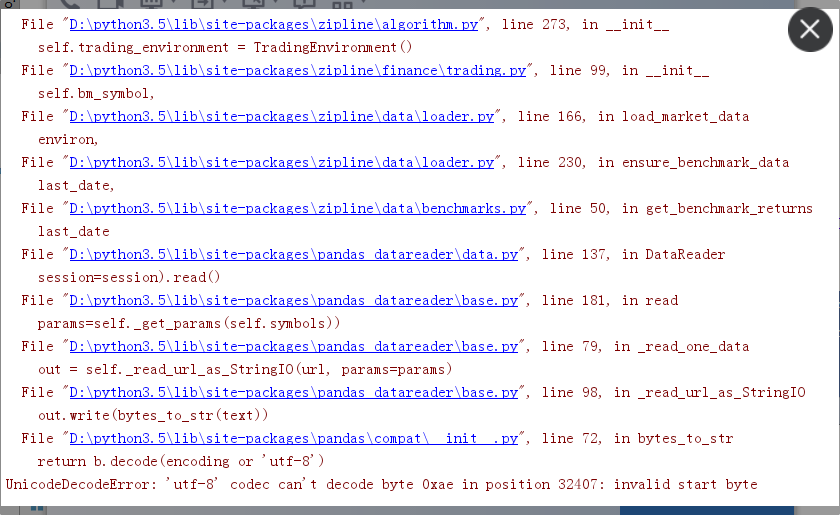

改写原因:在这个模块中的 get_benchmark_returns() 方法回去谷歌财经下载对应SPY(类似于上证指数)的数据,但是Google上下载的数据在最后写入Io操作的时候会报一个恶心的编码的错误,很烦人,时好时坏的那种,就是图下这种报错。

改写方式:

1.首先去雅虎财经下载SPY.csv文件,然后把这个文件放到你对应的目录下

2.具体代码如下

#

# Copyright 2013 Quantopian, Inc.

#

# Licensed under the Apache License, Version 2.0 (the "License");

# you may not use this file except in compliance with the License.

# You may obtain a copy of the License at

#

# http://www.apache.org/licenses/LICENSE-2.0

#

# Unless required by applicable law or agreed to in writing, software

# distributed under the License is distributed on an "AS IS" BASIS,

# WITHOUT WARRANTIES OR CONDITIONS OF ANY KIND, either express or implied.

# See the License for the specific language governing permissions and

# limitations under the License.

import numpy as np

import pandas as pd

import pytz

from datetime import datetime

import pandas_datareader.data as pd_reader

def get_benchmark_returns(symbol, first_date, last_date):

"""

Get a Series of benchmark returns from Google associated with `symbol`.

Default is `SPY`.

Parameters

----------

symbol : str

Benchmark symbol for which we're getting the returns.

first_date : pd.Timestamp

First date for which we want to get data.

last_date : pd.Timestamp

Last date for which we want to get data.

The furthest date that Google goes back to is 1993-02-01. It has missing

data for 2008-12-15, 2009-08-11, and 2012-02-02, so we add data for the

dates for which Google is missing data.

We're also limited to 4000 days worth of data per request. If we make a

request for data that extends past 4000 trading days, we'll still only

receive 4000 days of data.

first_date is **not** included because we need the close from day N - 1 to

compute the returns for day N.

"""

# 源码

# data = pd_reader.DataReader(

# symbol,

# 'google',

# first_date,

# last_date

# )

#

# data = data['Close']

#

# data[pd.Timestamp('2008-12-15')] = np.nan

# data[pd.Timestamp('2009-08-11')] = np.nan

# data[pd.Timestamp('2012-02-02')] = np.nan

#

# data = data.fillna(method='ffill')

# return data.sort_index().tz_localize('UTC').pct_change(1).iloc[1:]

# 自己写的代码

# parse = lambda x: pytz.utc.localize(datetime.strptime(x, '%Y-%m-%d'))

# data = pd.read_csv("SPY.csv", parse_dates=['Date'], index_col=0, date_parser=parse)

# data = data['Close']

# data = data.fillna(method='ffill')

# return data.sort_index().pct_change(1).iloc[0:]

总结:

1.这次报错后,我习惯性的找到最底层也就是最后两行错误,但是只能知道是编码的错误,但是解决不了。所以以后碰到类似的第三方包的错误,不要急着从最底层开始改,应该适当的想想,我在最开始出错的地方可不可以成功的避免掉,这也是一种思路。

2.Google财经的SPY数据不全,所以他在这个方法中定义了三列是因为这三天的数据他没有。