原文链接:http://tecdat.cn/?p=2841

此示例显示MATLAB如何从复合条件均值和方差模型预测 和条件差异。

步骤1加载数据并拟合模型

加载工具箱附带的纳斯达克数据。将条件均值和方差模型拟合到数据中。

-

-

nasdaq = DataTable.NASDAQ;

-

r = price2ret(nasdaq);

-

N = length(r);

-

-

model = arima('ARLa gs' 1,'Variance',garch(1,1),...

-

'Distrib ution','t');

-

fit = estimate(mode ,r,'Variance0',{'Constant0',0.001});

-

-

ARIMA(1,0,0) Model (t Distribution):

-

-

Value StandardError TStatistic PValue

-

_________ _____________ __________ __________

-

-

Constant 0.0012326 0.00018163 6.786 1.1528e-11

-

AR{1} 0.066389 0.021398 3.1026 0.0019182

-

DoF 14.839 2.2588 6.5693 5.0539e-11

-

-

-

-

GARCH(1,1) Conditional Variance Model (t Distribution):

-

-

Value StandardError TStatistic PValue

-

__________ _____________ __________ __________

-

-

Constant 3.4488e-06 8.3938e-07 4.1087 3.9788e-05

-

GARCH{1} 0.82904 0.015535 53.365 0

-

ARCH{1} 0.16048 0.016331 9.8268 8.6333e-23

-

DoF 14.839 2.2588 6.5693 5.0539e-11

-

[E0,V0] = infer(fit,r);

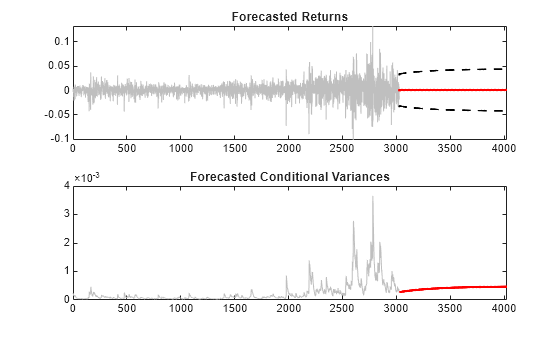

第2步预测收益和条件差异

使用forecast计算回报状语从句:条件方差为1000周期的未来视界的MMSE预测。使用观察到的回报和推断残差以及条件方差作为预采样数据。

-

[Y,YMS E,V] = forecast(fit, 100 0,'Y 0',r,'E0', E0, 'V0' ,V0);

-

upper = Y + 1.96*sqrt(YMSE);

-

lower = Y - 1.96*sqrt(YMSE);

-

-

figure

-

subplot(2,1,1)

-

plot(r,'Color',[.75,.75,.75])

-

hold on

-

plot(N+1:N+1000,Y,'r','LineWidth',2)

-

plot(N+1:N+1000,[upper,lower],'k--','LineWidth',1.5)

-

xlim([0,N+1000])

-

title('Forecasted Returns')

-

hold off

-

subplot(2,1,2)

-

plot(V0,'Color',[.75,.75,.75])

-

hold on

-

plot(N+1:N+1000,V,'r','LineWidth',2);

-

xlim([0,N+1000])

-

title('Forecasted Conditional Variances')

-

hold off

条件方差预测收敛于GARCH条件方差模型的渐近方差。预测的收益收敛于估计的模型常数(AR条件均值模型的无条件均值)。