序列变点检测在金融气象等领域的应用十分广泛。最近我在分析表观遗传数据的时候也用到了这项功能,当然是基于R语言进行分析的。

下面给出一个简单的使用示例。

- 安装cpm包。

install.packages("cpm") #初次使用需安装,以后就不需要了

library(cpm)

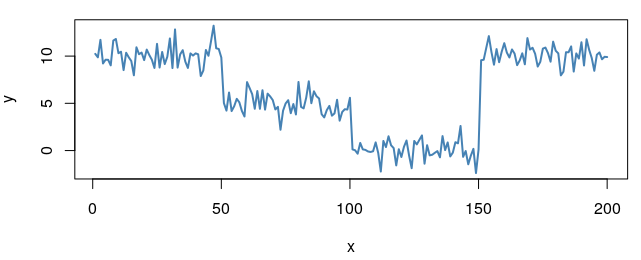

- 产生示例数据,并可视化查看数据。

df <- data.frame(x = 1:200, y = c(rnorm(50, 10), rnorm(50, 5), rnorm(50, 0), rnorm(50, 10)))

par(mfrow = c(2,1))

plot(df, type = "l", col = "steelblue", lwd = 2)

- 很明显,我们这里有三个非常明显的change point。

在这里说明下,如果你是要检测单个change point的话,应该使用detectChangePoint函数,但是在这个实例里,我们显然是想检测出多个,此时应该使用processStream函数。

processStream函数的cpmType参数的值有很多,主要有以下几种,

| Arguments | Condition |

|---|---|

| Student | Gaussian sequence |

| Bartlett | Gaussian sequence |

| GLR | Gaussian sequence |

| Exponential | Exponentially distributed sequence |

| GLRAdjusted; ExponentialAdjusted | Identical to the GLR and Exponential statistics |

| FET | Bernoulli sequence |

| Mann-Whitney | non-Gaussian distribution |

| Mood | non-Gaussian distribution |

| Lepage | non-Gaussian distribution |

| Kolmogorov-Smirnov | non-Gaussian distribution |

| Cramer-von-Mises | non-Gaussian distribution |

shapiro.test(df$y) #检验数据是否服从高斯分布,发现不服从。所以选择一个非高斯分布的方法使用

# Shapiro-Wilk normality test

# data: df$y

# W = 0.89808, p-value = 1.899e-10

cpm.res = processStream(df$y, cpmType = "Kolmogorov-Smirnov")

# 可视化变点

plot(df, type = "l", col = "steelblue", lwd = 2)

abline(v = cpm.res$changePoints, lwd = 3.5, col = "red")

# 变点坐标信息提取

print(cpm.res$changePoints)

# [1] 50 100 150