分位数回归及其Python源码

天朗气清,惠风和畅。赋闲在家,正宜读书。前人文章,不得其解。代码开源,无人注释。你们不来,我行我上。废话少说,直入主题。o( ̄︶ ̄)o

我们要探测自变量 与因变量

的关系,最简单的方法是线性回归,即假设:

我们通过最小二乘方法 (OLS: ordinary least squares), 的可靠性问题,我们同时对残差

做了假设,即:

为均值为0,方差恒定的独立随机变量。

即为给定自变量

下,因变量

的条件均值。

假如残差 不满足我们的假设,或者更重要地,我们不仅仅想要知道

的在给定

下的条件均值,而且想知道是条件中位数(更一般地,条件分位数),那么OLS下的线性回归就不能满足我们的需求。分位数回归(Quantile Regression)[2]解决了这些问题,下面我先给出一个分位数回归的实际应用例子,再简述其原理,最后再分析其在Python实现的源代码。

1. 一个例子:收入与食品消费

这个例子出自statasmodels:Quantile Regression.[3] 我们想探索家庭收入与食品消费的关系,数据出自working class Belgian households in 1857 (the Engel data).我们用Python包statsmodels实现分位数回归。

1.1 预处理

%matplotlib inline

import numpy as np

import pandas as pd

import statsmodels.api as sm

import statsmodels.formula.api as smf

import matplotlib.pyplot as plt

data = sm.datasets.engel.load_pandas().data

data.head()

income foodexp

0 420.157651 255.839425

1 541.411707 310.958667

2 901.157457 485.680014

3 639.080229 402.997356

4 750.875606 495.560775

1.2 中位数回归 (分位数回归的特例,q=0.5)

mod = smf.quantreg('foodexp ~ income', data)

res = mod.fit(q=.5)

print(res.summary())

QuantReg Regression Results

==============================================================================

Dep. Variable: foodexp Pseudo R-squared: 0.6206

Model: QuantReg Band 64.51

Method: Least Squares Sparsity: 209.3

Date: Mon, 21 Oct 2019 No. Observations: 235

Time: 17:46:59 Df Residuals: 233

Df Model: 1

==============================================================================

coef std err t P>|t| [0.025 0.975]

------------------------------------------------------------------------------

Intercept 81.4823 14.634 5.568 0.000 52.649 110.315

income 0.5602 0.013 42.516 0.000 0.534 0.586

==============================================================================

The condition number is large, 2.38e+03. This might indicate that there are

strong multicollinearity or other numerical problems.

由结果可以知道 ,如何得到回归系数的估计?结果中的std err, t, Pseudo R-squared等是什么?我会在稍后解释。

1.3 数据可视化

我们先拟合10个分位数回归,分位数q分别在0.05到0.95之间。

quantiles = np.arange(.05, .96, .1)

def fit_model(q):

res = mod.fit(q=q)

return [q, res.params['Intercept'], res.params['income']] +

res.conf_int().loc['income'].tolist()

models = [fit_model(x) for x in quantiles]

models = pd.DataFrame(models, columns=['q', 'a', 'b', 'lb', 'ub'])

ols = smf.ols('foodexp ~ income', data).fit()

ols_ci = ols.conf_int().loc['income'].tolist()

ols = dict(a = ols.params['Intercept'],

b = ols.params['income'],

lb = ols_ci[0],

ub = ols_ci[1])

print(models)

print(ols)

q a b lb ub

0 0.05 124.880096 0.343361 0.268632 0.418090

1 0.15 111.693660 0.423708 0.382780 0.464636

2 0.25 95.483539 0.474103 0.439900 0.508306

3 0.35 105.841294 0.488901 0.457759 0.520043

4 0.45 81.083647 0.552428 0.525021 0.579835

5 0.55 89.661370 0.565601 0.540955 0.590247

6 0.65 74.033435 0.604576 0.582169 0.626982

7 0.75 62.396584 0.644014 0.622411 0.665617

8 0.85 52.272216 0.677603 0.657383 0.697823

9 0.95 64.103964 0.709069 0.687831 0.730306

{'a': 147.47538852370562, 'b': 0.48517842367692354, 'lb': 0.4568738130184233,

这里拟合了10个回归,其中q是对应的分位数,a是斜率,b是回归系数。lb和ub分别是b的95%置信区间的下界与上界。

现在来画出这10条回归线:

x = np.arange(data.income.min(), data.income.max(), 50)

get_y = lambda a, b: a + b * x

fig, ax = plt.subplots(figsize=(8, 6))

for i in range(models.shape[0]):

y = get_y(models.a[i], models.b[i])

ax.plot(x, y, linestyle='dotted', color='grey')

y = get_y(ols['a'], ols['b'])

ax.plot(x, y, color='red', label='OLS')

ax.scatter(data.income, data.foodexp, alpha=.2)

ax.set_xlim((240, 3000))

ax.set_ylim((240, 2000))

legend = ax.legend()

ax.set_xlabel('Income', fontsize=16)

ax.set_ylabel('Food expenditure', fontsize=16);

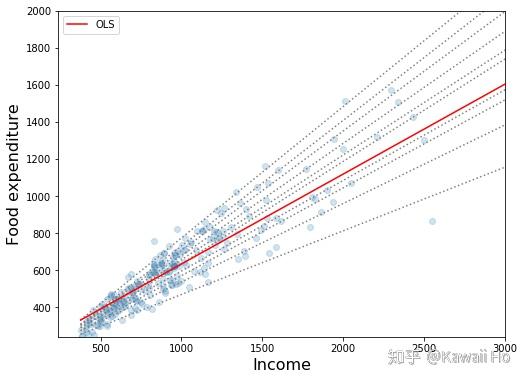

上图中虚线是分位数回归线,红线是线性最小二乘(OLS)的回归线。通过观察,我们可以发现3个现象:

- 随着收入提高,食品消费也在提高。

- 随着收入提高,家庭间食品消费的差别拉大。穷人别无选择,富人能选择生活方式,有喜欢吃贵的,也有喜欢吃便宜的。然而我们无法通过OLS发现这个现象,因为它只给了我们一个均值。

- 对与穷人来说,OLS预测值过高。这是因为少数的富人拉高了整体的均值,可见OLS对异常点敏感,不是一个稳健的模型。

2.分位数回归的原理

这部分是数理统计的内容,只关心如何实现的朋友可以略过。我们要解决以下这几个问题:

- 什么是分位数?

- 如何求分位数?

- 什么是分位数回归?

- 分位数回归的回归系数如何求得?

- 回归系数的检验如何进行?

- 如何评估回归拟合优度?

2.1 分位数的定义]

是随机变量,

的累积密度函数是

.

的

分位数为:

,

假设有100个人,95%的人身高少于1.9m, 1.9m就是身高的95%分位数。

2.2 分位数的求法

通过选择不同的 值,使

最小,对应的

值即为

的

分位数的估计

.

2.3 分位数回归

对于OLS, 我们有:

为

最小化所对应的

,类比地,对于

分位数回归,我们有:

为最小化:

即最小化

所对应的

2.4 系数估计

由于 不能直接对

求导,我们只能用迭代的方法来逼近

最小时对应的

值。statsmodels采用了Iteratively reweighted least squares (IRLS)的方法。

假设我们要求 最小化形如下的

范数:

则第t+1步迭代的 值为:

是对角矩阵且初始值为

第t次迭代

以中位数回归为例子(q=0.5),我们求:

即

即最小化形如上的 范数,

为避免分母为0,我们取 ,

是一个很小的数,例如0.0001.

2.5 回归系数的检验

我们通过2.4,多次迭代得出 的估计值,为了得到假设检验的t统计量,我们只需得到

的方差的估计。

分位数回归

的协方差矩阵的渐近估计为:

其中 是对角矩阵,

当 ,

, 当

,

的估计为

其中

为核函数(Kernel),可取Epa,Gaussian等.

为根据Stata 12所选的窗宽(bandwidth)[5]

回归结果中的std err即由 获得,t统计量等于

。

2.6 拟合优度

对于OLS,我们用 来衡量拟合优度。对于

分位数回归,我们类比得到:

,其中

为所有

观察值的

分位数。

即为回归结果中的Pseudo R-squared。

3.Python源码分析

实现分位数回归的完整源码在 ,里面主要含有两个类QuantReg 和 QuantRegResults. 其中QuantReg是核心,包含了回归系数估计,协方差计算等过程。QuantRegResults计算拟合优度并组织回归结果。

3.1 QuantReg类

#QuantReg是包中RegressionModel的一个子类

class QuantReg(RegressionModel):

#计算回归系数及其协方差矩阵。q是分位数,vcov是协方差矩阵,默认robust即2.5的方法。核函数kernel默认

#epa,窗宽bandwidth默认hsheather.IRLS最大迭代次数默认1000,差值默认小于1e-6时停止迭代

def fit(self, q=.5, vcov='robust', kernel='epa', bandwidth='hsheather',

max_iter=1000, p_tol=1e-6, **kwargs):

"""

Solve by Iterative Weighted Least Squares

Parameters

----------

q : float

Quantile must be between 0 and 1

vcov : str, method used to calculate the variance-covariance matrix

of the parameters. Default is ``robust``:

- robust : heteroskedasticity robust standard errors (as suggested

in Greene 6th edition)

- iid : iid errors (as in Stata 12)

kernel : str, kernel to use in the kernel density estimation for the

asymptotic covariance matrix:

- epa: Epanechnikov

- cos: Cosine

- gau: Gaussian

- par: Parzene

bandwidth : str, Bandwidth selection method in kernel density

estimation for asymptotic covariance estimate (full

references in QuantReg docstring):

- hsheather: Hall-Sheather (1988)

- bofinger: Bofinger (1975)

- chamberlain: Chamberlain (1994)

"""

if q < 0 or q > 1:

raise Exception('p must be between 0 and 1')

kern_names = ['biw', 'cos', 'epa', 'gau', 'par']

if kernel not in kern_names:

raise Exception("kernel must be one of " + ', '.join(kern_names))

else:

kernel = kernels[kernel]

if bandwidth == 'hsheather':

bandwidth = hall_sheather

elif bandwidth == 'bofinger':

bandwidth = bofinger

elif bandwidth == 'chamberlain':

bandwidth = chamberlain

else:

raise Exception("bandwidth must be in 'hsheather', 'bofinger', 'chamberlain'")

#endog样本因变量,exog样本自变量

endog = self.endog

exog = self.exog

nobs = self.nobs

exog_rank = np.linalg.matrix_rank(self.exog)

self.rank = exog_rank

self.df_model = float(self.rank - self.k_constant)

self.df_resid = self.nobs - self.rank

#IRLS初始化

n_iter = 0

xstar = exog

beta = np.ones(exog_rank)

# TODO: better start, initial beta is used only for convergence check

# Note the following does not work yet,

# the iteration loop always starts with OLS as initial beta

# if start_params is not None:

# if len(start_params) != rank:

# raise ValueError('start_params has wrong length')

# beta = start_params

# else:

# # start with OLS

# beta = np.dot(np.linalg.pinv(exog), endog)

diff = 10

cycle = False

history = dict(params = [], mse=[])

#IRLS迭代

while n_iter < max_iter and diff > p_tol and not cycle:

n_iter += 1

beta0 = beta

xtx = np.dot(xstar.T, exog)

xty = np.dot(xstar.T, endog)

beta = np.dot(pinv(xtx), xty)

resid = endog - np.dot(exog, beta)

mask = np.abs(resid) < .000001

resid[mask] = ((resid[mask] >= 0) * 2 - 1) * .000001

resid = np.where(resid < 0, q * resid, (1-q) * resid)

resid = np.abs(resid)

#1/resid[:, np.newaxis]为更新权重W

xstar = exog / resid[:, np.newaxis]

diff = np.max(np.abs(beta - beta0))

history['params'].append(beta)

history['mse'].append(np.mean(resid*resid))

#检查是否收敛,若收敛则提前停止迭代

if (n_iter >= 300) and (n_iter % 100 == 0):

# check for convergence circle, should not happen

for ii in range(2, 10):

if np.all(beta == history['params'][-ii]):

cycle = True

warnings.warn("Convergence cycle detected", ConvergenceWarning)

break

if n_iter == max_iter:

warnings.warn("Maximum number of iterations (" + str(max_iter) +

") reached.", IterationLimitWarning)

#计算协方差矩阵

e = endog - np.dot(exog, beta)

# Greene (2008, p.407) writes that Stata 6 uses this band

# h = 0.9 * np.std(e) / (nobs**0.2)

# Instead, we calculate bandwidth as in Stata 12

iqre = stats.scoreatpercentile(e, 75) - stats.scoreatpercentile(e, 25)

h = bandwidth(nobs, q)

h = min(np.std(endog),

iqre / 1.34) * (norm.ppf(q + h) - norm.ppf(q - h))

fhat0 = 1. / (nobs * h) * np.sum(kernel(e / h))

if vcov == 'robust':

d = np.where(e > 0, (q/fhat0)**2, ((1-q)/fhat0)**2)

xtxi = pinv(np.dot(exog.T, exog))

xtdx = np.dot(exog.T * d[np.newaxis, :], exog)

vcov = chain_dot(xtxi, xtdx, xtxi)

elif vcov == 'iid':

vcov = (1. / fhat0)**2 * q * (1 - q) * pinv(np.dot(exog.T, exog))

else:

raise Exception("vcov must be 'robust' or 'iid'")

#用系数估计值和协方差矩阵创建一个QuantResults对象,并输出结果

lfit = QuantRegResults(self, beta, normalized_cov_params=vcov)

lfit.q = q

lfit.iterations = n_iter

lfit.sparsity = 1. / fhat0

lfit.bandwidth = h

lfit.history = history

return RegressionResultsWrapper(lfit)

#核函数表达式

def _parzen(u):

z = np.where(np.abs(u) <= .5, 4./3 - 8. * u**2 + 8. * np.abs(u)**3,

8. * (1 - np.abs(u))**3 / 3.)

z[np.abs(u) > 1] = 0

return z

kernels = {}

kernels['biw'] = lambda u: 15. / 16 * (1 - u**2)**2 * np.where(np.abs(u) <= 1, 1, 0)

kernels['cos'] = lambda u: np.where(np.abs(u) <= .5, 1 + np.cos(2 * np.pi * u), 0)

kernels['epa'] = lambda u: 3. / 4 * (1-u**2) * np.where(np.abs(u) <= 1, 1, 0)

kernels['gau'] = lambda u: norm.pdf(u)

kernels['par'] = _parzen

#kernels['bet'] = lambda u: np.where(np.abs(u) <= 1, .75 * (1 - u) * (1 + u), 0)

#kernels['log'] = lambda u: logistic.pdf(u) * (1 - logistic.pdf(u))

#kernels['tri'] = lambda u: np.where(np.abs(u) <= 1, 1 - np.abs(u), 0)

#kernels['trw'] = lambda u: 35. / 32 * (1 - u**2)**3 * np.where(np.abs(u) <= 1, 1, 0)

#kernels['uni'] = lambda u: 1. / 2 * np.where(np.abs(u) <= 1, 1, 0)

#窗宽计算

def hall_sheather(n, q, alpha=.05):

z = norm.ppf(q)

num = 1.5 * norm.pdf(z)**2.

den = 2. * z**2. + 1.

h = n**(-1. / 3) * norm.ppf(1. - alpha / 2.)**(2./3) * (num / den)**(1./3)

return h

def bofinger(n, q):

num = 9. / 2 * norm.pdf(2 * norm.ppf(q))**4

den = (2 * norm.ppf(q)**2 + 1)**2

h = n**(-1. / 5) * (num / den)**(1. / 5)

return h

def chamberlain(n, q, alpha=.05):

return norm.ppf(1 - alpha / 2) * np.sqrt(q*(1 - q) / n)

3.2 QuantRegResults类

这里我只给出计算拟合优度的代码。

class QuantRegResults(RegressionResults):

'''Results instance for the QuantReg model'''

@cache_readonly

def prsquared(self):

q = self.q

endog = self.model.endog

#e为残差

e = self.resid

e = np.where(e < 0, (1 - q) * e, q * e)

e = np.abs(e)

ered = endog - stats.scoreatpercentile(endog, q * 100)

ered = np.where(ered < 0, (1 - q) * ered, q * ered)

ered = np.abs(ered)

return 1 - np.sum(e) / np.sum(ered)

4.总结

上文我先给出了一个分位数回归的应用例子,进而叙述了分位数回归的原理,最后再分析了Python实现的源码。

分位数回归对比起OLS回归,虽然较为复杂,但它有三个主要优势:

- 能反映因变量分位数与自变量的关系,而不仅仅反映因变量均值与自变量的关系。

- 分位数回归对残差不作任何假设。

- 分位数回归受异常点的影响较小。

参考

- ^https://en.wikipedia.org/wiki/Ordinary_least_squares

- ^QUANTILE REGRESSION http://www.econ.uiuc.edu/~roger/research/rq/rq.pdf

- ^https://www.statsmodels.org/dev/examples/notebooks/generated/quantile_regression.html

- [1](https://www.zhihu.com/#ref_4_0)bchttps://en.wikipedia.org/wiki/Quantile_regression

- [2](https://www.zhihu.com/#ref_5_0)bchttps://www.statsmodels.org/devel/_modules/statsmodels/regression/quantile_regression.html

- ^https://en.wikipedia.org/wiki/Iteratively_reweighted_least_squares

- ^Green,W. H. (2008). Econometric Analysis. Sixth Edition. International Student Edition.

- ^https://www.ibm.com/support/knowledgecenter/en/SSLVMB_sub/statistics_mainhelp_ddita/spss/regression/idh_quantile.html